If you’re using (or considering) a SIMPLE IRA (Savings Incentive Match Plan for Employees IRA), one of your top questions will be: what are the contribution limits for 2025? Contribution rules matter because they affect how much you can save each year, how much your employer may be required to contribute, and how to avoid mistakes that could lead to penalties or compliance issues.

This guide explains the SIMPLE IRA contribution limits for 2025 in a practical, step-by-step way. You’ll learn about employee elective deferrals, catch-up contributions (including when they apply), employer matching limits, and key deadlines that usually determine how your contributions count. simple ira contribution limits 2025 We’ll also cover common scenarios—like part-year employment, age-based catch-up, and multiple retirement accounts—to help you plan accurately.

1) What Is a SIMPLE IRA?

A SIMPLE IRA is a retirement plan designed mainly for small businesses. It allows eligible employees to make salary deferrals (employee contributions), while the employer typically makes a required contribution in the form of either:

- Matching contributions (common approach), or

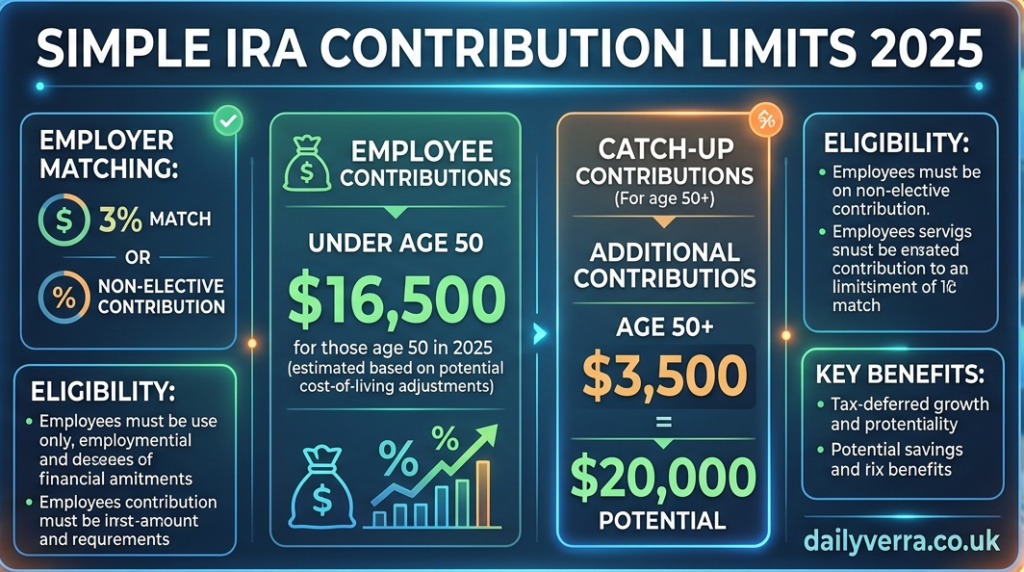

- Non-elective contributions (a flat contribution made to employees)

The simple ira contribution limits 2025 generally offers a simpler setup than many other retirement plans (like a 401(k)), but it still has specific rules about who can participate and how much can be contributed each year.

2) SIMPLE IRA Employee Contribution Limits for 2025

A) Employee elective deferrals (regular limit)

The core contribution most employees make to a simple ira contribution limits 2025 is called an elective deferral (often just called “employee contributions” in everyday language). For 2025, the SIMPLE IRA employee contribution limit is determined by the IRS annual deferral limit.

In most years, this limit applies to your contributions through payroll (or through allowed contributions during the plan year if the plan allows it). If you exceed the limit, your contributions may need corrective distribution actions depending on how the excess is handled by the plan administrator.

B) Catch-up contributions (age 50+)

If you are age 50 or older, you may qualify for an additional catch-up contribution amount. Catch-up contributions are designed to help older workers save more as they approach retirement.

For simple ira contribution limits 2025, the catch-up contribution generally applies when you reach the age threshold by a specific point in the year (commonly based on age during the calendar year).

Practical tip:

If you’ll turn 50 during 2025, you should confirm exactly when the plan starts treating you as eligible for catch-up. Many employers handle this through their payroll system once you meet eligibility.

C) Total employee limit (regular + catch-up)

Your total employee elective deferrals for 2025 are usually the sum of:

- The regular elective deferral limit, plus

- Any catch-up amount you qualify for (if eligible)

This matters because your payroll withholding should stop automatically once you hit the allowed limit, but it’s still your responsibility to monitor it with your pay stub totals and the plan’s reporting simple ira contribution limits 2025.

3) Employer Contributions in a SIMPLE IRA (Matching / Non-Elective)

Employee contributions are only part of the story. A simple ira contribution limits 2025 plan typically requires employer contributions, and these employer amounts can be significant.

A) Employer matching contributions (common structure)

If your employer uses the matching method, the employer generally matches your elective deferrals according to a required formula set by law (within the SIMPLE IRA rules).

In general, SIMPLE IRA matching contributions are designed so that employees receive employer support to encourage participation and savings.

B) Non-elective employer contributions

Some employers use a non-elective contribution approach, which is a flat employer contribution made regardless of whether you defer salary—again, subject to the plan’s conditions and legal requirements.

C) Employer contribution limits (for 2025)

While employees have a specific deferral limit, employer contributions also follow annual rules and maximums. These limits can affect total plan contributions for the year simple ira contribution limits 2025.

Important:

You should treat the employer contribution as separate from your personal elective deferrals. simple ira contribution limits 2025 Your employer might contribute even if you make a low deferral—or no deferral—depending on whether your plan uses matching or non-elective rules.

4) How to Calculate Your 2025 Contribution Amount (Practical Examples)

Let’s turn the rules into something you can actually use. Because the exact dollar amounts for 2025 depend on IRS inflation adjustments, the cleanest approach is to calculate using the official 2025 limits and your payroll schedule simple ira contribution limits 2025.

Example 1: You contribute a fixed amount each paycheck

Suppose you’re paid biweekly (26 paychecks per year). If you plan to contribute X dollars per paycheck, then:

- Total employee elective deferrals in 2025 = 26×X

To avoid exceeding the limit, 26×X should be at or below the 2025 employee elective deferral limit (plus catch-up, if eligible).

Example 2: You start mid-year

If you begin participating later in 2025 (for example, you were hired in March), you have fewer pay periods remaining simple ira contribution limits 2025.

A simple method:

- Estimate how many paychecks remain in 2025 after your start date

- Divide the remaining limit by remaining paychecks to determine a safe per-paycheck amount

Example conceptually:

- Remaining employee limit ÷ remaining paychecks = per-paycheck amount

Example 3: Age 50 catch-up later in the year

If you’ll turn 50 in 2025, your contributions may need to be structured carefully so that you don’t accidentally exceed the regular limit before catch-up eligibility begins.

A practical approach:

- Track total deferrals each payroll

- Ask payroll/HR when catch-up begins for you under the plan rules

- Adjust the paycheck contribution amount accordingly

5) Deadlines: When Do 2025 SIMPLE IRA Contributions Count?

Even if you contribute during 2025, the plan’s operational rules and employer processing timing determine what counts for the tax year.

Typically, payroll contributions that are withheld during the year are counted for that year, simple ira contribution limits 2025 but some plans allow additional contributions based on IRS rules and the employer’s plan setup.

What you should do:

- Confirm with your plan administrator or HR how they handle contribution timing

- Watch how they report year-end totals

- Keep your own payroll records (or at least quarterly summaries)

6) Can You Contribute to Other Retirement Accounts Too?

Yes, in most cases you can also contribute to other retirement accounts such as:

- Roth IRA / Traditional IRA

- 401(k) (if you have access elsewhere)

- SEP IRA (typically not for employees in the same way)

- Solo 401(k) (if self-employed)

However, the presence of other retirement accounts does not automatically raise your SIMPLE IRA limits. Each plan generally has its own annual restrictions simple ira contribution limits 2025.

Common confusion:

People sometimes assume that if they max out their SIMPLE IRA, they can still “keep adding” to reach other limits. But SIMPLE IRA has its own annual cap for employee deferrals (and separate rules for employer contributions).

7) Who Is Eligible for a SIMPLE IRA?

Eligibility is one of the main administrative requirements. simple ira contribution limits 2025 participation rules generally depend on:

- How long you’ve worked for the employer (the plan and IRS rules specify conditions)

- Whether you meet minimum service requirements

- Age requirements may apply to employer contributions in some scenarios

Your employer should provide plan documents describing eligibility dates and enrollment procedures.

8) Withdrawals, Taxes, and Penalties (Quick Overview)

Even though your question is about contribution limits, it’s smart to know what happens later.

A) Withdrawals are generally taxable

SIMPLE IRA withdrawals are typically subject to income tax as ordinary income.

B) Early withdrawal penalty may apply

If you withdraw before reaching the applicable age threshold, you may face additional penalties depending on the rules and holding period.

C) Holding period matters

For simple ira contribution limits 2025, the penalty rules can be different if you haven’t met the required holding period for penalty exceptions.

Practical note:

Before making withdrawals or transfers, review plan rules or ask a tax professional because early withdrawals can be expensive.

9) Common Mistakes to Avoid with SIMPLE IRA Contribution Limits

Here are the most common “limit-related” problems people run into:

- Over-contributing due to payroll timing errors or delayed adjustments

- Not accounting for catch-up properly if you are 50+

- Assuming employer matching is automatic even when you are not making deferrals (depends on plan type)

- Forgetting that multiple payroll runs may cause you to reach the limit earlier than expected

- Not reviewing year-end statements to confirm correct totals

Best practices:

- Confirm your expected total contributions before year-end

- Periodically check your pay stubs and year-to-date retirement deductions

- Keep an eye on HR/plan communication about limit changes for the year

10) How to Prepare Your 2025 Savings Plan

If your goal is to maximize your retirement contributions responsibly, use this checklist:

Step 1: Find your 2025 SIMPLE IRA employee limits

Look up the official IRS limit for 2025 and the catch-up amount (if applicable).

Step 2: Determine your contribution rate

Decide an amount per paycheck that will get you close to the limit without exceeding it.

Step 3: Confirm catch-up eligibility timing (if age 50+)

If you qualify, confirm when catch-up begins.

Step 4: Understand employer contributions

Know whether your plan uses:

- matching contributions, or

- non-elective contributions

Step 5: Track and adjust

If your payroll contributions are set monthly or biweekly, you may need adjustments based on your remaining pay periods.

11) Quick Reference Summary (What Matters Most)

When people ask about simple ira contribution limits 2025, the key items they usually need are:

- Employee elective deferral limit for 2025

- Catch-up contribution amount (if age 50+)

- Employer matching/non-elective contribution requirements

- Total annual contribution structure and limit considerations

- Operational timing and deadlines

- Avoiding excess contributions and correction issues

12) Final Thoughts

A simple ira contribution limits 2025 is often one of the easiest ways to build retirement savings, especially if you want a streamlined plan with clear rules. simple ira contribution limits 2025 But to make the most of it, you should plan around the annual contribution limits and ensure payroll deductions are aligned with your eligibility and timing for 2025.

If you want, tell me:

- your age (or whether you’ll be 50+ in 2025),

- whether your employer uses matching or non-elective contributions, and

- your pay frequency (weekly/biweekly/monthly),

and I’ll help you estimate a safe per-paycheck contribution amount to stay within the simple ira contribution limits 2025 while maximizing your savings.